Producer Pay Forecast: March 31, 2026

Markets are sending mixed signals as we head into Spring. Milk production continues to trend higher in the U.S and internationally. Dairy product inventories remain near or below prior year levels for commodities like butter and cheese, while nonfat dry milk stocks have fallen well below prior year due to minimal production.

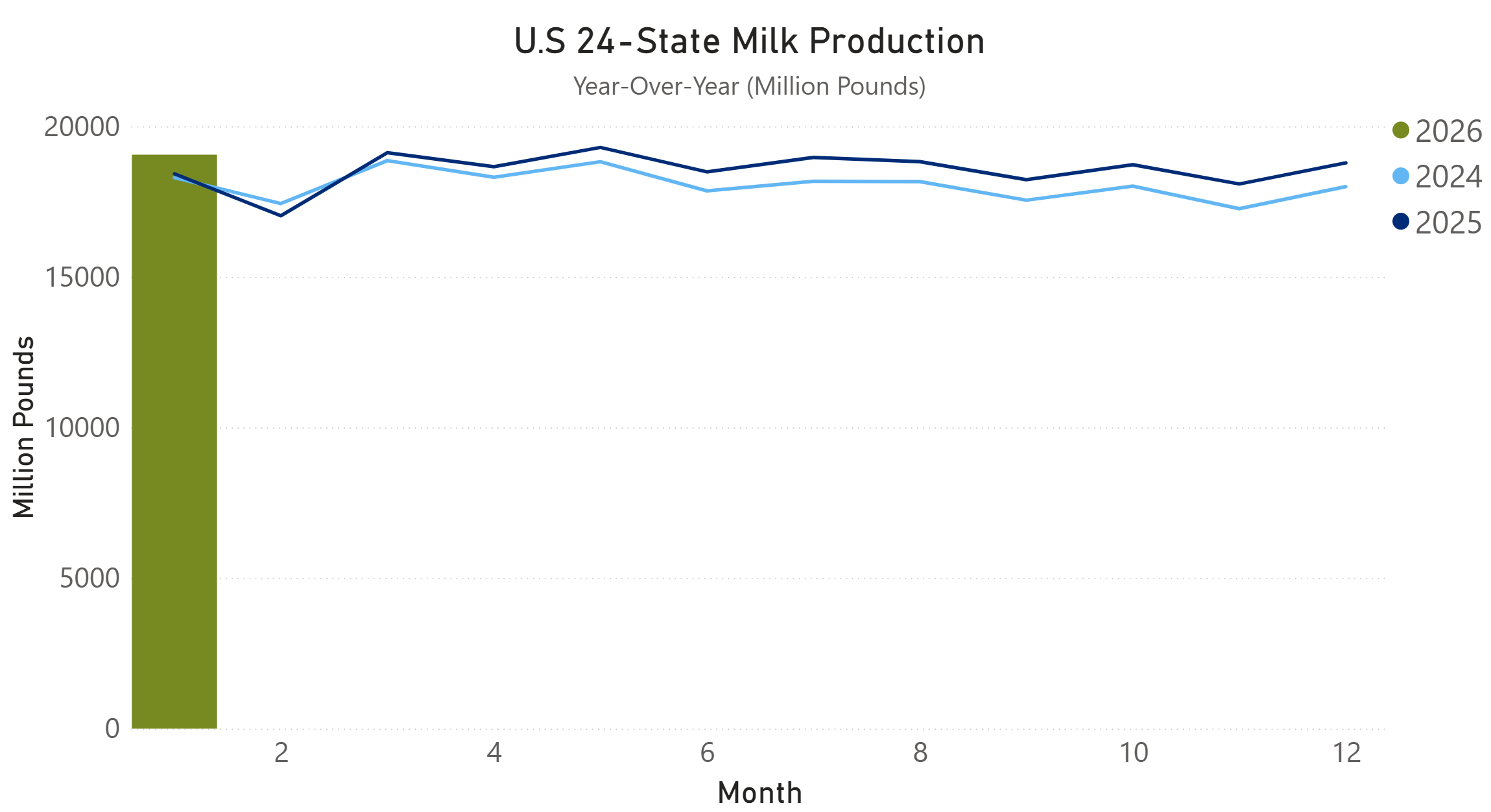

- 24-state milking herd grew 2.4% year-over-year in February.

- U.S milk production grew more than 3% over the same period.

- Butter stocks reached 253.8 million pounds in February, building seasonally but still more than 10% below the five-year average.

- Total cheese stocks were down a modest 1% Y-o-Y in February. February nonfat dry milk stocks were down 28.7% Y-o-Y.

Growth in milk production will likely moderate in the coming months as we lap last year's expansion, but overall supply growth is expected to remain elevated.

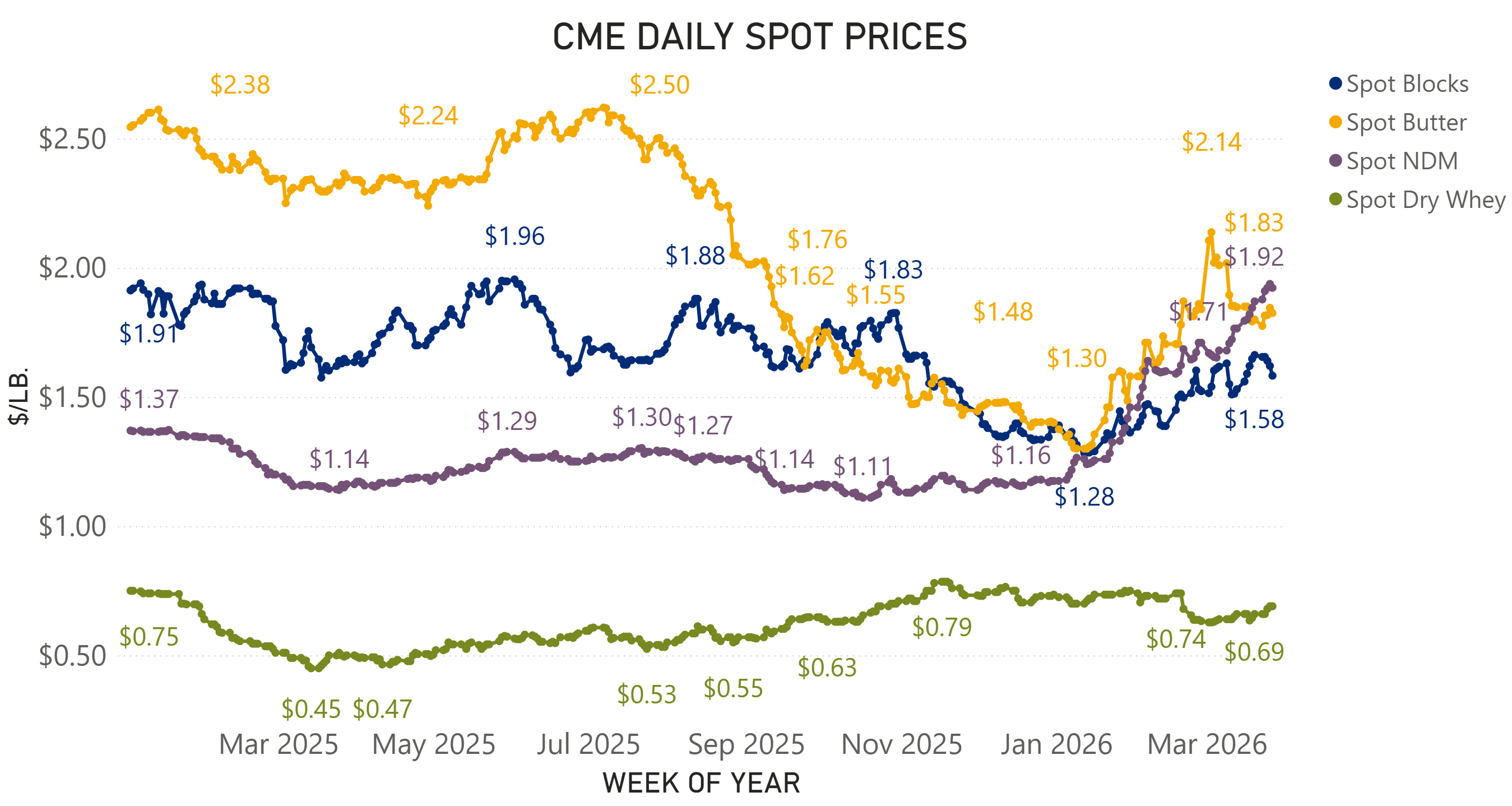

CME spot markets are reflecting these current conditions. Cheese prices have gained some support, while nonfat dry milk continues to climb towards $2.00/lb. Dry whey prices have returned to the high $0.60's, while butter searches for stability, spending the last two weeks in the $1.70's-$1.80's.

Average $/lb. week ending 3/27/2026:

- Blocks: $1.63

- Butter: $1.82

- Dry whey: $0.68

- NDM: $1.91

While reportedly tight butter stocks indicate support for butter prices as we move through the second half of the year, cream availability will be a key watch point. Markets are better supported today than in recent months, but that can shift . Strong domestic demand will become increasingly more important to absorb additional supply as exports remain a concern for the U.S.