Producer Pay Forecast: February 24, 2026

The dairy market seems to be transitioning from a prolonged oversupply environment toward gradual rebalancing, though structural supply pressures remain significant.

Milk production continues to run well above prior-year levels, with global milk output keeping pace alongside the U.S.

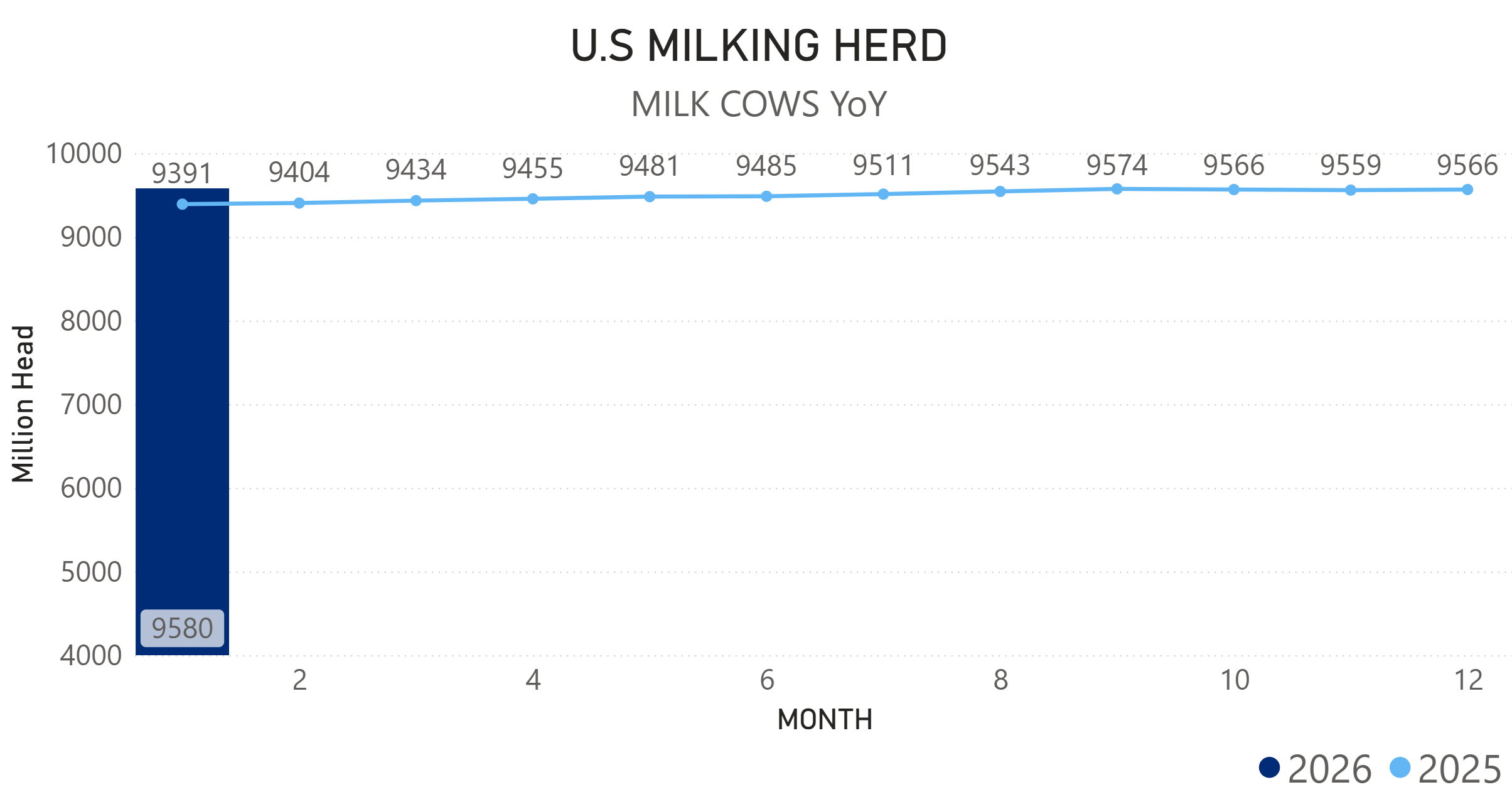

- 24-State U.S milk production grew 3.45% (YoY January)

- U.S milking herd expanded to 9.5 million, up 2.23% (YoY January)

- 24-State U.S milk per cow rose 1.17% (YoY January)

Growth seems to be driven primarily by herd expansion and productivity gains. In New York, milk production grew 3.4%, reflecting a 3.7% growth in herd size despite slightly lower milk per cow (YoY January).

Culling activity increased sharply to begin 2026, with week 1 up 36.73% (YoY), before moderating and averaging 6.05% over the following four weeks. Despite the uptick, the U.S milking herd remains historically large. Anecdotal reports and new USDA data also suggest that producers have begun pulling back on palm-based feed additives in response to prolonged oversupply and continued global milk production growth.

These factors have the ability to limit future supply expansion, although they are unlikely to drive rapid contraction in the near-term. Continued strength in exports, increased domestic demand, or further reduction in butterfat output could accelerate market tightening.

Cold Storage:

January cold storage data revealed mixed inventory trends.

Butter stocks down 17.4% YoY, but up 27.78 million pounds MoM

Total cheese stocks up 1.8% YoY, and up 2.35 million pounds MoM

This indicates butter inventories remain tight relative to last year despite seasonal rebuilding, while cheese stocks remain generally balanced when compared to current production levels.

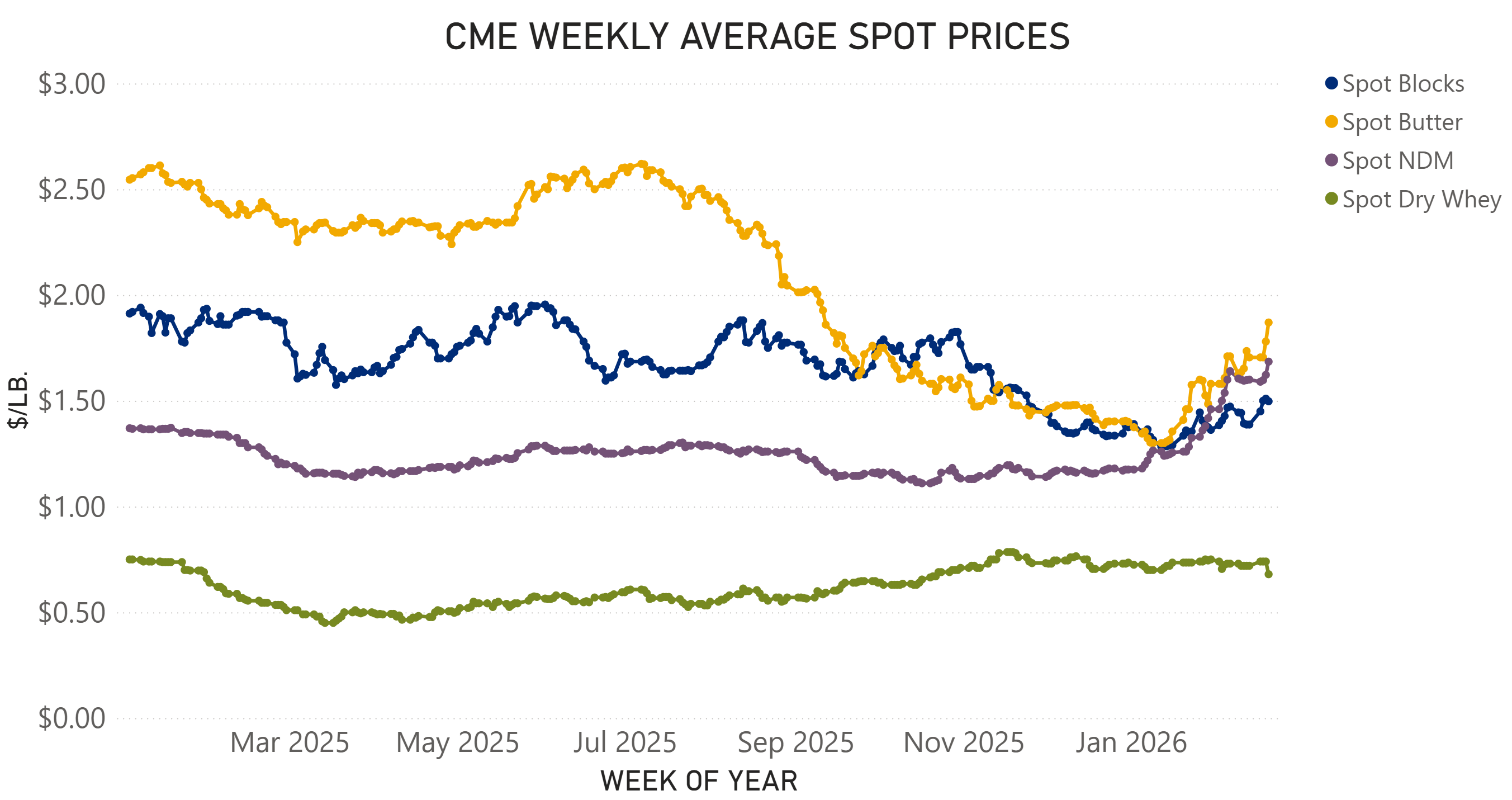

CME Spot Market Prices—February 24, 2026:

- Blocks $1.5600/lb.

- Butter $1.8125/lb.

- NDM $1.6500/lb.

- Dry Whey $0.6375/lb.

Spot markets strengthened modestly in mid-February, before slightly easing again at the start of this week, reflecting reports of tightening butterfat availability alongside reactions to USDA's announcement of Section 32 purchases. Through AMS, the USDA released plans to purchase $148 million in dairy products, including $75 million in butter, which could provide a meaningful near-term demand boost. Further details of these purchases have not been released.

As U.S prices strengthen, export competitiveness remains a key concern. Dry whey prices have declined over the last week, likely reflecting global competition, with New Zealand whey currently averaging $0.64/lb. and European whey around $0.55/lb., and low domestic demand.

Record U.S dairy exports in 2025 helped to prevent a severe inventory buildup despite the significant global supply growth. However, as domestic prices rise, U.S products may become less competitive internationally, particularly among nontraditional trade partners that drove recent export gains. Export competitiveness is therefore expected to act as a key constraint on the magnitude of price recovery throughout 2026.

As dairy markets appear to be rebounding slightly, butter markets are likely to lead the recovery due to reports of tightening butterfat availability and government purchases, while cheese prices may improve at a more gradual pace given continued high milk supply and ongoing protein trends.

Nonfat dry milk markets have strengthened significantly and remain above $1.60/lb., primarily due to reduced production as milk is diverted toward cheese plants and higher-value protein manufacturing. Export demand is not expected to increase meaningfully, and the current strength in prices is driven by tight supply rather than demand growth.

Overall, while early indicators suggest supply growth may be starting to moderate, significant uncertainty remains around underlying production capacity and global demand conditions. As a result, market rebalancing is expected to be gradual, with increased price volatility likely as competing supply and demand forces continue to evolve.

Please feel free to reach out to Allee at acoombe@uncdairy.com or by calling the Membership Office with any questions or to discuss markets!