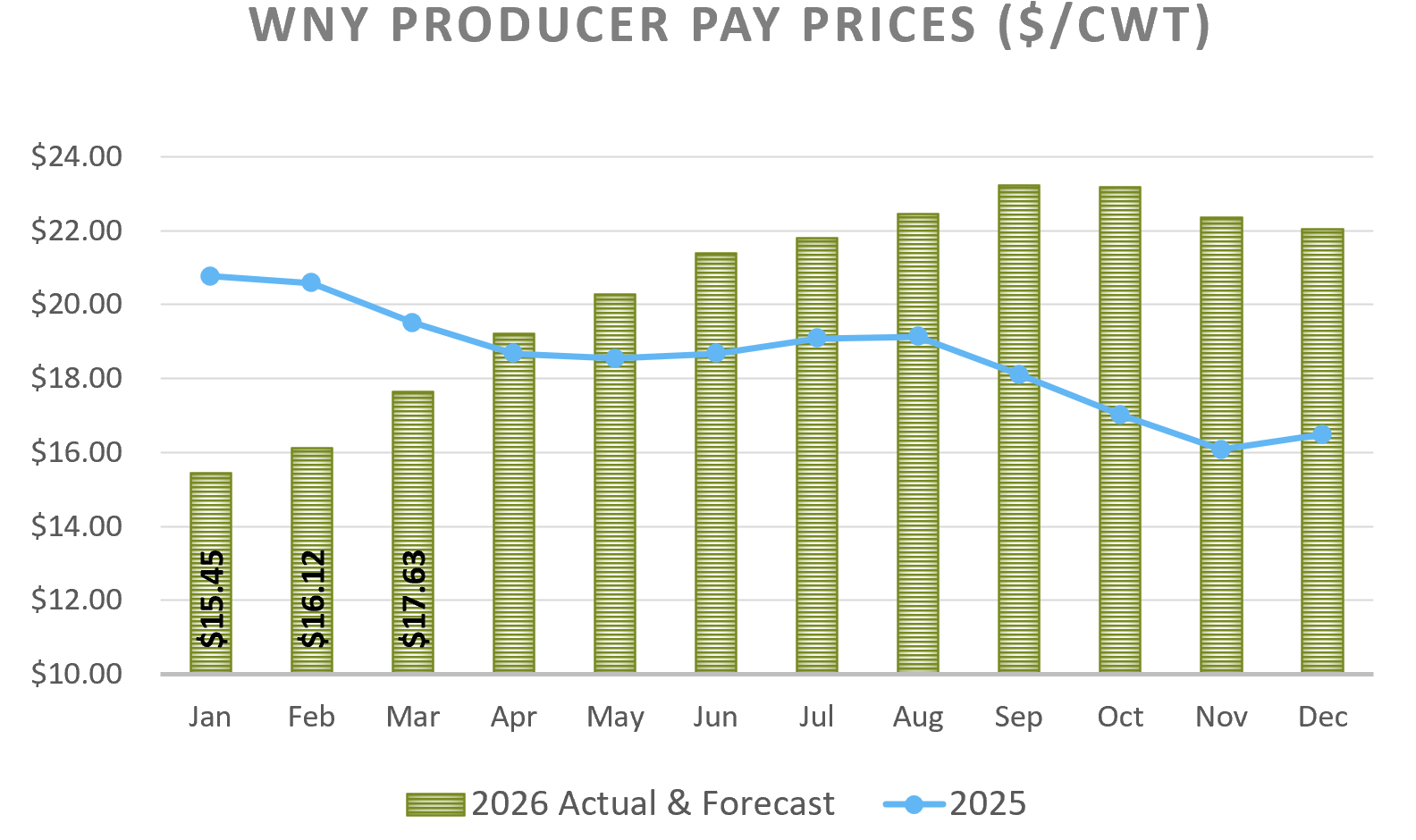

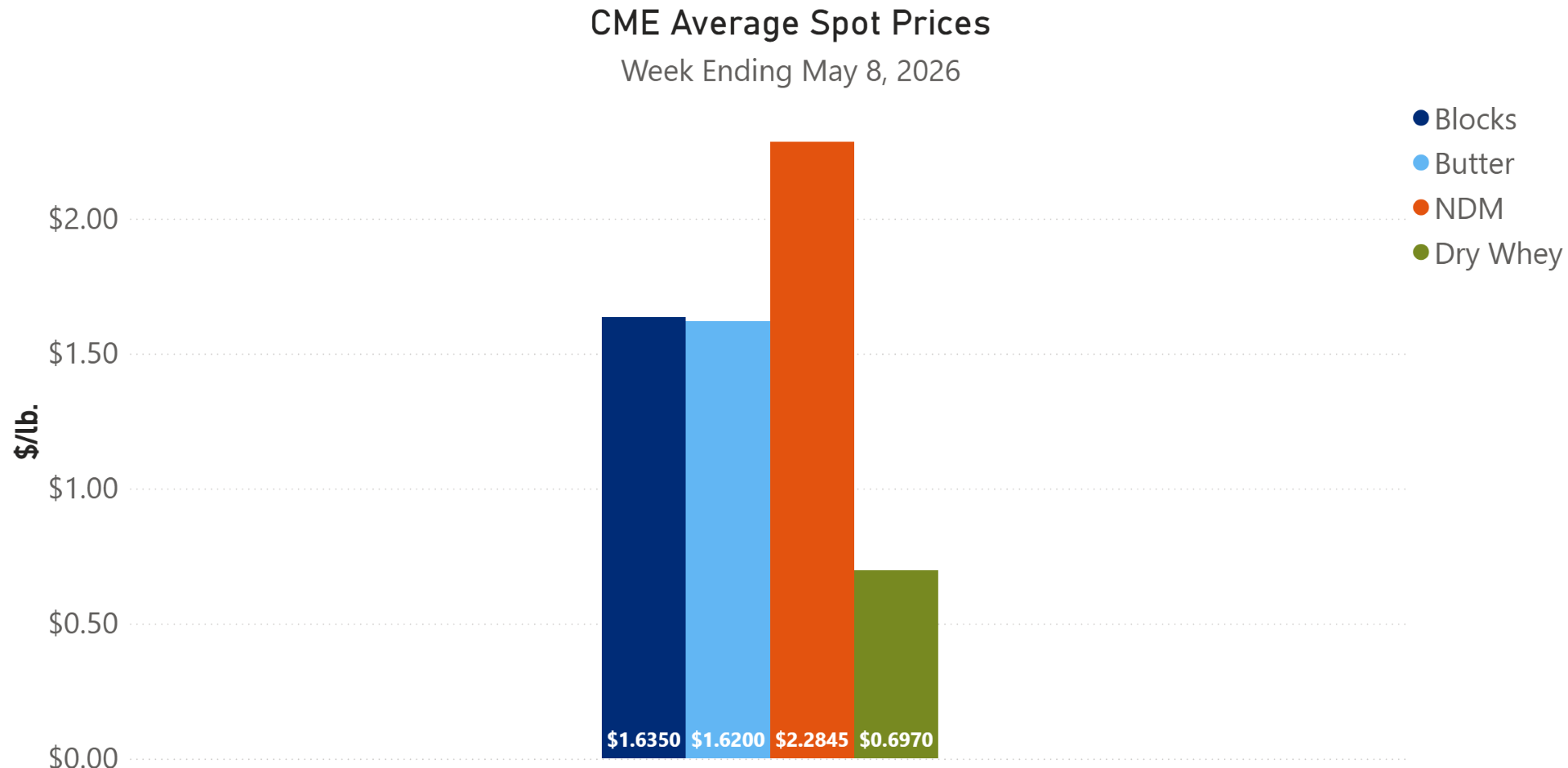

Producer Pay Forecast: May 8, 2026

Milk production continues to expand across the major export regions, but record U.S. cheese exports, strong butter shipments, and tighter year-over-year (YoY) inventories for these products are helping to absorb this heavier supply. The key risk is whether that balance holds if exports begin to slow, or input costs rise further.

Newly Released Data Points and Market Notes:

Milk Production & Herd

- 24-State milk production grew 2.44% (March YoY)

- U.S milking herd was up 2.09% (March YoY)

- NY milk production increased 2.1%, despite milk per cow being down 0.68% (March YoY)

- Dairy cattle slaughter is up 2.2% year-to-date(YTD) through March

Dairy Products:

- American-Cheddar production was down 2% (March YoY), but up 7.9% month-over-month

- American cheese inventories came in 2.55% below prior year for March

- Total cheese stocks fell 1.64% (March YoY)

- U.S. cheese exports created another new record in March at 140 million pounds, up more than 28% YoY

- Cottage curd production grew 19% (March YoY)

- Gouda production grew 43.9% (March YoY)

- Butter production was up 1.2% (March YoY), and has grown 7.05% YTD through March

- Butter stocks were down 10.6% (March YoY)

- Butter exports were up 86% (March YoY)

- Nonfat dry milk production increased 9.9% (March YoY)

- Nonfat dry milk stocks fell 10.3% (March YoY)

- Dry whey production increased 3.5% (March YoY)

Herd expansion across the U.S. is contributing heavily to production growth, reaching 9.183 million head in March. While milk and components keep flowing, their end-use has evolved. Cheese production has taken supply away from the dryers in 2026 to meet increasingly higher demand for high protein whey products. As demand grew for whey protein concentrate 80+ and whey protein isolate, cheese began relying more consistently on exports for supply absorption. Nonfat dry milk experienced an extended period of low production leading to record breaking spot prices. Global NDM/SMP production is beginning to pick back up, and as European and New Zealand prices come down, the U.S. must follow to maintain export competitiveness. Butter exports have remained strong and domestic demand is steady, but with production up across the globe, the U.S. must maintain a price gap with the EU and NZ to ensure our product remains the first choice.

Due to this evolving market, Class IV has continued trading above Class III, and stronger Class II demand is increasing the competition for cream supplies. Producer pay prices are receiving support as a result.

As always, please feel free to reach out with any questions or discussion!