Producer Pay Forecast: October 15, 2025

We are heading into the new year with more questions than certainties. Due to the government shutdown, we will not have any updates to share regarding September milk production, August and September dairy products production, or September stock levels. These reports will hopefully be published retroactively by USDA when the shutdown ends.

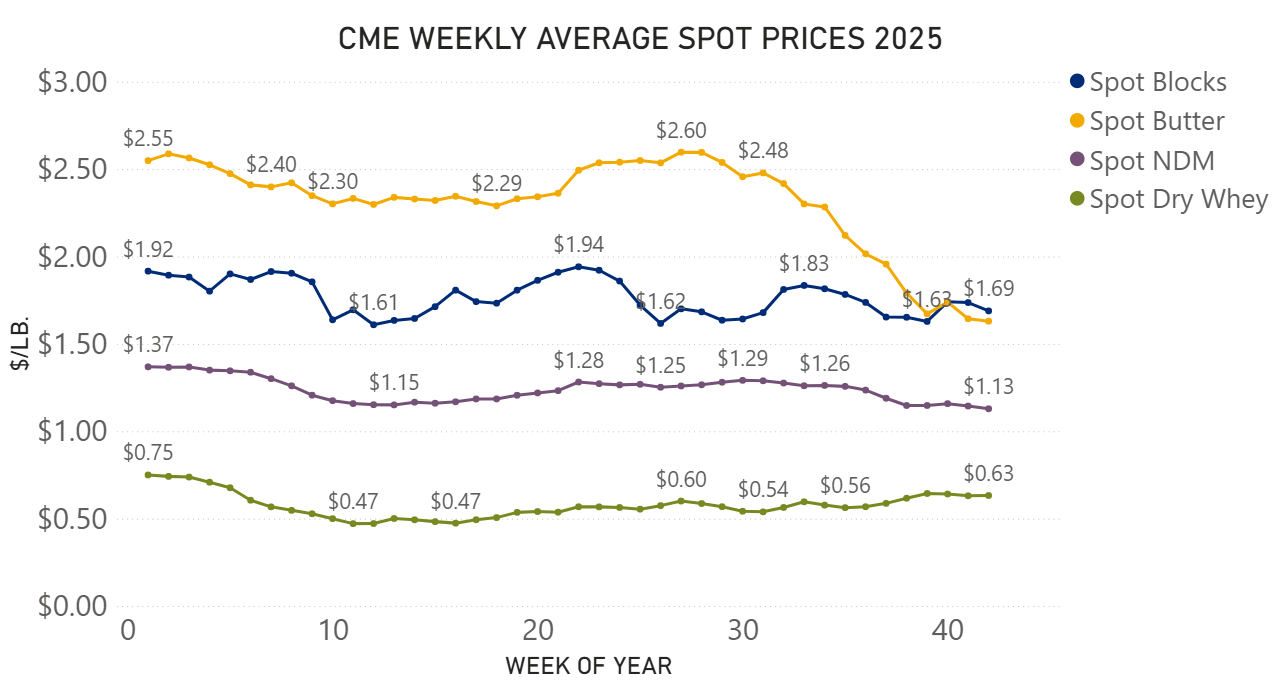

This forecast reflects current market realities and trends. The market remains heavy with milk and cream, keeping downward pressure on butter and Class IV values. Cheese prices are beginning to soften as well, bringing Class III values down. Interestingly, dry whey is experiencing an uptick in prices, offering some welcome support to Class III values.

While we anticipate a gradual firming in butter prices toward the end of the first quarter of 2026, it is unclear if the commodity has reached its floor. The possibility of butter falling below $1.60/lb. by year-end 2025 is not out of the question as reports of excess supply continue. Cheese and NDM prices are also forecast to ease before making a gradual improvement through the second half of 2026. A sustained recovery for the U.S dairy market will ultimately depend on export performance and domestic demand over the coming months, as the industry searches for a balance between production and utilization.

Global supply remains robust, with both Europe and New Zealand increasing their own outputs, adding competitive pressure on U.S exports. The abundant milk supply within the U.S and internationally, combined with healthy global competition, and sluggish domestic demand suggest a slow start to 2026 as the market works to rebalance supply and demand.

Please feel free to reach out to Allee at acoombe@uncdairy.com with any questions or concerns about the forecast or market trends as we navigate the months ahead.